Last year, our team put together a timeline of events for 20 cancer early detection (EDx) companies focused on blood-based approaches*. We chose these players due to their innovation, progress, and potential. However, a number of other, exciting competitors may ultimately be top contenders. We have continued tracking the space over the last year and are excited to share our findings (updates included through mid-October 2022). In this post, we evaluate 2021-2022 EDx developments, emerging players and key technical differentiators, and geographic findings.

Key 2021-2022 EDx Developments

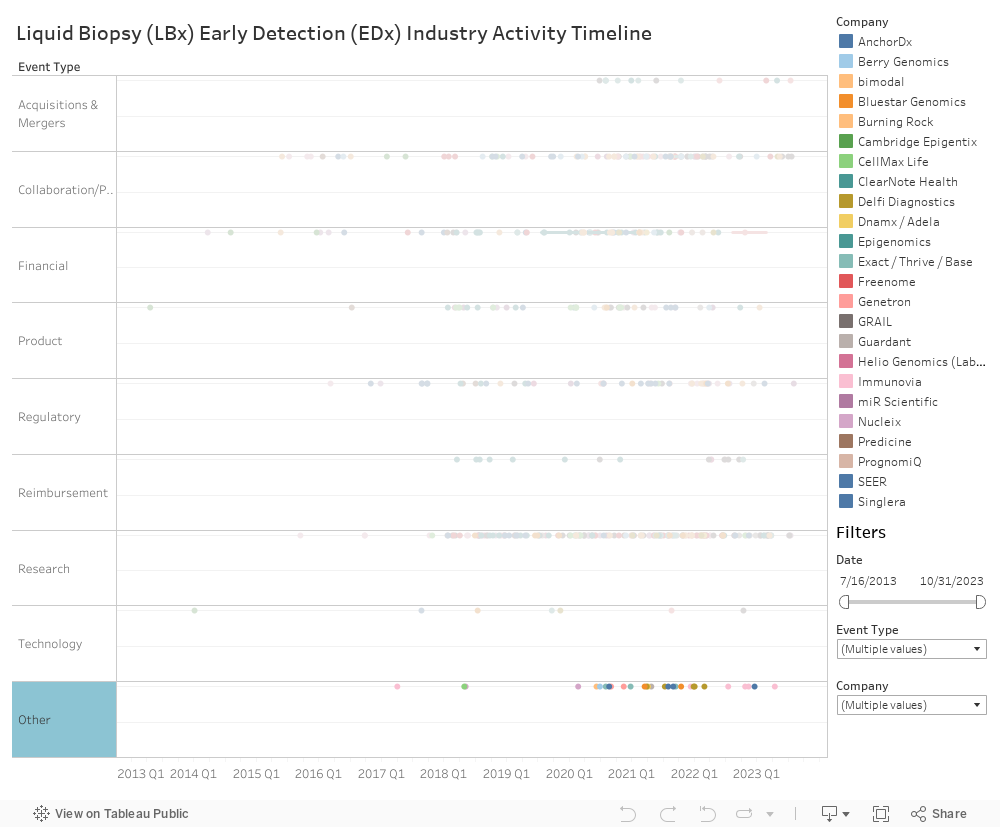

Figure 1: Cancer Early Detection - Updated Timeline* of Select Key Events

Cancer early detection continues to excite with notable developments like new product launches and initial insurance coverage. Since last year, the biggest overall changes to the EDx landscape include Guardant Health launching SHIELD CRC, Berry Genomics launching HIFI, a multi-cancer EDx, and some private insurance beginning to cover cancer early detection. Other noteworthy activity involves regulatory milestones and capital raises. AnchorDx’s Pulmoseek and Burning Rock’s OverC received CE markings, and CellMax Life’s blood test received FDA Breakthrough Device Designation. Financial investments (e.g., Delfi’s $225M Series C Funding, Freenome’s $290M investment by Roche to surpass $1B in total funding) fuel research and development. Ongoing, massive clinical trials (e.g., Freenome’s PREEMPT CRC study with 35K participants, Guardant’s SHIELD Lung study with 10K participants) are testing these products’ performance and clinical utility. Some have already released promising results (e.g., GRAIL’s PATHFINDER study). Early preliminary trial results are expected to snowball into more clinical-stage investments that will help drive blood-based EDx test validation over the next ~5 years. However, to drive investments, companies will need to likely enroll large (>15k) patient groups in order to capture significant positive cancer cases across various indications.**

Emerging Players and Key Technical Differentiators

Figure 2: Noteworthy Company Developments*

While established players still battle head-to-head, newer market entrants are fighting for a seat at the table. Some newer names (e.g., Geneseeq) have already released promising data. Other well-known oncology diagnostic providers like Natera, a leader in MRD, are slowly edging their way into early detection. While significant developments have been made over the past few years, the field is still in early-stages. As seen before, some companies capitalize on specific technologies while others leverage multiple technology types (i.e., multi-omics) to optimize performance. Due to perceived advantages of these multiple, competing technologies, the EDx space is becoming increasingly saturated. Catching up to top competitors that are developing high performing assays and have initiated large-scale clinical trials is a challenge for new market entrants. With so many companies in the space, venture capital funding is a land grab. Furthermore, large and long clinical trials exacerbate capital funds needed and delay product timelines. Nevertheless, given the unpredictability surrounding EDx development, the final winners have yet to emerge.

Figure 3: Other Noteworthy and Newer Early Detection Players*

In waging bets on who these winners may be, it is critical to consider whether detecting single or multiple indications is the best approach from both a strategic and technological standpoint. The top companies spread across multi-cancer early detection (MCED) and single cancer early detection (SCED), but often pursue both. SCED offers high value in optimizing a cancer detection algorithm for single cancer types. MCED expands diagnostic potential in ambiguous / hypothesis-free circumstances and into indications where no substantial screening methods exist today. However, it has drawbacks in that optimizing for one cancer type in MCED comes at the expense of others. Overtime, some cannibalization of single-cancer testing is expected mid- to long-term as MCED approaches become increasingly sensitive and specific.

Figure 4: SCED vs. MCED Approaches by Company

Geographic Findings

Last year, we noted increasing overlap of the EDx landscape into China. Looking forward, we expect even more Chinese involvement in both the U.S. and EU. Recent regulatory milestones include CE markings for Burning Rock and SeekIn. Global clinical trials and partnerships will promote further expansion. However, any testing in China requires a local laboratory presence. This stipulation tapers some Chinese expansion and can increase barriers for ex-Chinese company activity, furthering the need for partnership.

Figure 5: APAC’s Growing EDx Market

Additional Insights and Further Research

With developments over the year, new and ongoing questions that we have include:

1. Which technologies will win (ctDNA, methylation, etc)?

Hypothesis: Early cancer detection has shown growth with different technologies, but it is still too early to discover the best approach. Companies show promise by detecting methylation, ctDNA, and even RNA. Ultimately, multi-omic approaches may optimize performance of multiple approaches, but added workflow complexities and increased product premiums may taper global scalability near-term.

2. How will trials incorporate diversity to improve accuracy?

Hypothesis: Companies are recognizing that clinical trial diversification can improve algorithm powered technologies to optimize performance. President Biden’s Cancer Moonshot sparked heightened political interest towards cancer detection and furthers diversification incentives. Studies like GRAIL’s PATHFINDER 2 aim to accurately reflect U.S. demographics with regards to racial, ethnical, and sexual representation. These efforts make trial recruitment difficult but may increase diagnostic efficacy. This article written by members of our team highlights how inclusion and diversity in precision medicine can improve algorithms overall and be pivotal to success.

3. What will the path to reimbursement look like? How critical will this be to adoption?

Hypothesis: Expansion of coverage is critical to ensuring widespread test access and to ultimately improve cancer care overall. Likely, the U.S. will be a leader in securing reimbursement, while the E.U. may require 3+ years to catch up. As an intermediate step, some companies are partnering with private insurance to provide some test coverage (e.g., GRAIL’s partnerships including Foundation Health, Henry Ford Health, and Carrum Health Partner). FDA approvals may accelerate reimbursement realization. Trial durations are dependent on reaching a statistically significant number of cancer diagnoses, lending extensive trial periods especially for lower incident cancers. Designing clever clinical trials (e.g., incorporating real world data) may be one strategy used in the future to accelerate time to FDA approval. Nevertheless, FDA approval alone does not guarantee CMS coverage. For example, Epigenomics AG’s Epi proColon(R) CRC blood-based EDx test is FDA approved but not covered by CMS. Rather, the U.S. Preventive Services Task Force (USPSTF), an evidence-based organization that guides physicians in clinical prevention, is critical, though it unfortunately has a history of long update cycles (~5 years) that can lag biomedical innovation. The Patient Protection and Affordable Care Act (ACA) necessitates stricter CMS alignment with USPSTF guidelines. Ultimately, the USPSTF incorporation of blood-based early detection into routine prevention guidelines can be turnkey for CMS coverage and ultimate success in altering patient prognosis.

Notes: * Companies highlighted on this timeline and in this article are not a comprehensive representation of all cancer early detection companies

** Around Q2 2022, Guardant and Freenome delayed trial readouts and significantly expanded patient enrollment, likely in order to fulfill trial designs with a pre-specified number of positive cancer cases to be captured

.png)

.png)