The cancer EDx landscape continues to evolve with multiple ongoing clinical trials, coverage announcements, companies expanding into new indications, and new entrants exploring novel modalities and analytes.

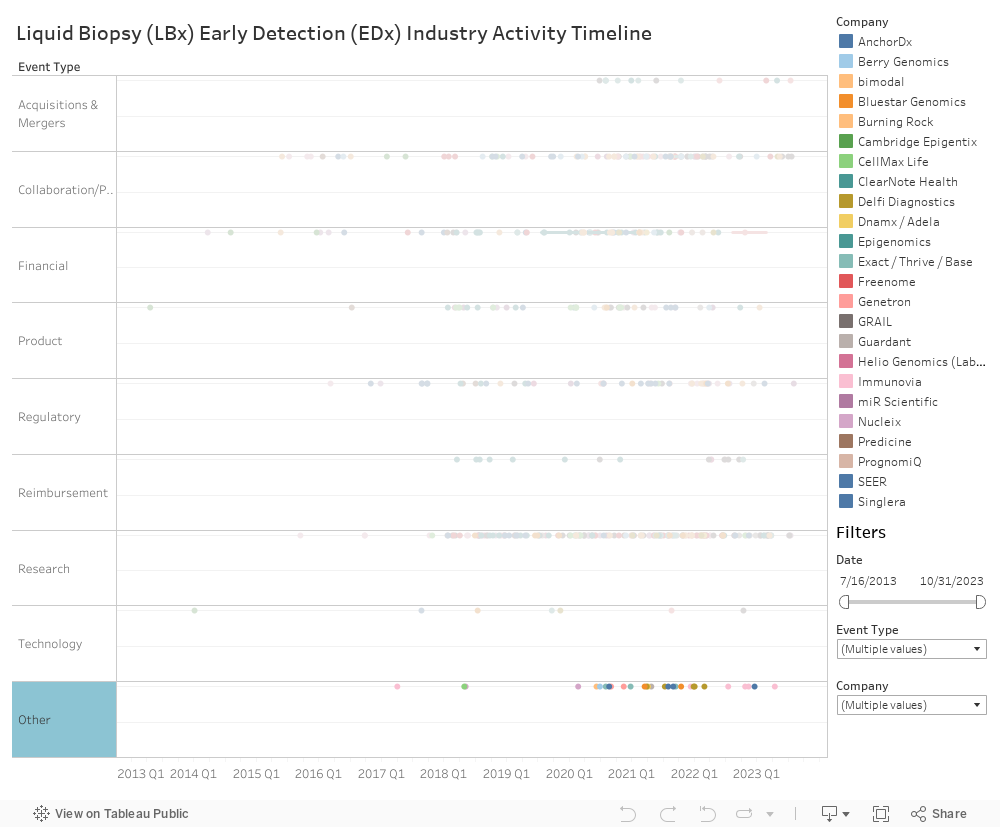

To monitor the rapidly-evolving market landscape, we have maintained an activity tracker covering the commercial, clinical, and regulatory activity for a selection of ~20 of these EDx companies (find 2021 updates here, find 2022 updates here). See the updated activity tracker below (updated through Q3 of 2023).

Figure 2: Cancer Early Detection - Updated Timeline of Select Key Events (Note: Companies highlighted on this timeline are not a comprehensive representation of all cancer early detection companies; these 20 are among those that come up most frequently in our discussions and research in the EDx space. Other prominent companies to be tracked throughout 2024 include Biological Dynamics, Geneseeq, Exai Bio, Harbinger Health, Mirxes, and Genecast.)

Given the nascency of the landscape, it is still undecided what the winning test approach and commercial strategy will look like. Our discussions with clinicians and KOLs reinforce that clinical performance (e.g., in the near term: sensitivity, specificity, positive predictive value, negative predictive value; in the long term: survival outcomes) is the most important determinant for success, up to a certain level. Beyond that threshold, other commercial parameters, such as cost / reimbursement, indication-specific utility (e.g., MCED vs. SCED assays), clinical decision support services and infrastructure, and marketing become differentiating.

To further assess the keys to success in the cancer EDx market, we interviewed a senior-level product stakeholder at a leading early cancer detection company to discuss the landscape, including key drivers, moderators, and risks for technology development and adoption moving forward. Please find a transcript of our discussion below:

(Disclaimer: These are the interviewee’s opinions and not necessarily reflective of DeciBio’s perspectives).

Considering the cancer early detection landscape, what are you most excited about for the coming one to two years?

Blood based CRC testing getting FDA approval and adoption in the clinic.

What do you think are the key drivers for early cancer detection adoption?

I think the main drivers are FDA approval, followed by reimbursement and guideline adoption. These will be necessary to see early cancer detection adopted on a broad basis. Given that these products will generally be used in an average risk population, there is a higher bar that needs to be met to gain approval. It is more challenging to achieve guideline incorporation and reimbursement coverage in this type of population versus a cancer patient population. I think these are the three key components that we are waiting to see realized across the board with any early cancer detection products.

What are key challenges the field is facing?

If we start from just the FDA approval, the clinical studies and the clinical evidence that are going to need to be generated and just the sheer size of those and then the investment that's required—those are still rate limiting. I mean, you see one of the major players pivoting a bit away from some of their more aggressive timelines and stance around their own set of products. I'm guessing that that's based on some of the feedback they've gotten from the FDA in terms of their expectations and requirements. Guardant recently made an investor day announcement around their own study that they're going to be initiating fairly soon. I haven't had a chance to fully dive into that and develop a perspective, but I'm sure there are some nuggets to unpack from that announcement as well.

There are a number of key players that are active in the space and that have initiated clinical trials or are in the middle of ongoing clinical trials. Clearly the space is becoming increasingly crowded. How do you expect that to shake out either over the near-term or midterm, and do you expect significant consolidation?

I'll start from the last part. Yes, I do because of our financial macro environment. It’s harder to fundraise, and there's more of a focus on path to profitability. So, I think because of that, there's going to be a big falling out. At the end of the day, a lot of these companies are just different technology plays, and so I think there's going to be some consolidation. Exact Sciences, as you know, has bought a lot of companies. I think there's going to be continuing M&A activity, companies unable to fundraise, and others running out of their runway. For example, some of those smaller players in the field have announced strategic repositioning and restructuring, and I imagine there will be more of those. To be candid, I'm surprised there haven't been more already. That’s just my theory. As I said before, the investment needed is not the same as a 510K where you can just show equivalency pathway. You’re always going to need these very large, expensive clinical studies. At some point, there will be enough solutions on market where there is not going to be investment into the next round and next round. At least, I don't think so, but I could be proven wrong.

And given that perspective that a lot are different technologies that are going after the same things- some of these companies are going after single indications versus others going after multi cancer indication approaches. What do you think are some of the drawbacks or benefits of either approach? And what are some of the key considerations that companies really evaluate when determining which paths or combinations to pursue?

First, with a single cancer approach, there can be more clarity in a path to adoption. I should even caveat that by saying that clarity only really exists in CRC where you have the NCD (national coverage determination) decision. You know what performance you need to achieve to gain FDA approval and coverage. Beyond that, as you look into a lot of these companies, they're going after lung as their next indication. There isn't that same clarity. So, I say that with a bit of a grain of salt.

MCED, on the other hand, is a whole other level of complexity. For example, GALLERI is really the only MCED on market, and they're still trying to figure out what the right use case is for it. In the U.S., it has been rolled out as an LDT for adults aged 50 and up who are considered an average risk population. Age is a risk factor, but this is generally an average risk population. They're running studies in symptomatic patients with their SYMPLIFI study. They also identified a use case around firefighters and related research being done in this group. They have the financial means to run these different studies to find a use case that works best.

I don't think there's a clear path to use or approval for the flavor of MCED we have. Someday we might expect an MCED “version 2” that is fundamentally different, but to me this will be about having a completely different performance level. The challenge with some MCEDs is the requirement for an average risk and a very high specificity, which means you sacrifice on sensitivity. At the end of the day, for screening or surveillance, you're trying to pick up cancer, and sensitivity is very important. Maybe there will be a “version 2” that can advance us past this limitation, but current technologies make identifying the right test application a challenge.

You touched on this already briefly, but obviously there's a balance between sensitivity and specificity. What are some of the disadvantages versus advantages of prioritizing each metric when developing a test?

It depends on the use case you're trying to go after, and what clinically makes sense. Generally speaking, MCEDs are limited because they target an average risk population and many cancer types. They must aim for that very high specificity and sacrifice sensitivity. Single cancer applications are almost the exact opposite because they largely aim to be used for screening. They must prioritize sensitivity and meet a clinically acceptable specificity, which can vary quite a bit depending on the target population. If you consider CRC screening, for example, you work with an average risk population and might have a somewhat higher or lower bar for specificity than with a lung screening population, who are higher risk. For cancers without routine screening practices, such as liver cancer or pancreatic cancer, what's clinically acceptable could be different still.

For early cancer detection tests, primary care physicians will typically be ordering the test. How do they typically respond when given information about this test? Are they excited about it? Are they hesitant to incorporate these tests into their clinical workup?

There’s probably no one answer to that. Based on some of the feedback I’ve heard, I'd say that there may be more skepticism now. Because of the experience and association with current tests, there is already some hesitation and an ingrained perception that will have to be overcome. There is some objection now to early cancer detection tests, even though many offerings can be for very different use cases other than the MCED approach.

I had a conversation with a PCP recently, and she mentioned discussing MCED with her colleagues and how to approach it now that patients are coming in and asking for these tests. Their decision was to ask if the patient had completed all recommended guideline screening. If the answer was no, their response would be to come back after completing all recommended screening and they could revisit MCED.

This conversation speaks to what’s really happening and the real-world scenario. When we get caught up in the hype of an MCED, a lot of people are not adherent or compliant across all the recommended cancer screenings. MCED is not intended to replace those, so recommended screening is really where PCPs need to focus their time and energy. They are also incentivized to do through HEDIS metrics in place to hit on certain targets for screening.

One thing that we discuss a lot internally is how companies are really focusing on incorporating diversity into their clinical trials. Obviously, sample cohorts that are more representative of the general population can better train an algorithm to address that population. How can these algorithm-based technologies be optimized by better incorporating trial diversity? How top-of-mind is sample diversity for companies developing these tests?

I’m not the subject matter expert on this topic, but I know the FDA has put out draft guidance around diversity in clinical studies. This is a great change for clinical studies. With the FDA taking that stance, diversity will be continuously and increasingly expected in trials. The guidance will help ensure we’re building products that are fit for the entire population and not just a subset of the population.

Another point when it comes to algorithms and algorithm development is that they are sensitive to diversity not only in your population but in other facets as well. It’s really important in R&D phases to consider diversity in the population, in addition to diversity amongst clinical sites and sample selection methods. Each of these factors have an impact on your algorithm development.

As a last question, broadly, is there anything that we haven't discussed thus far that you think is top of mind for the future of cancer early detection?

Reflecting on what we have discussed thus far, I hope that there's not a bubble created by all the excitement and energy around early cancer detection. I hope we don't burn ourselves or build a bad reputation based on the first, early offerings in the space. I hope the early results do not lead to a failure that pushes the field to move on to something else. Right now, our only options are GALLERI and Guardant. It will be interesting to see how the FDA responds to Guardant’s recent data and whether that may change the field’s trajectory.

I worry about the effect of all this hype with no proof to back it up. Ultimately, success will likely be pretty dependent onFDA approval. If Guardant receives restrictive labeling, that may cause loss of confidence. I hope that doesn't happen, because I think we still have a lot of improvement to make and a long way to go. We want to make it to see the“version 2.” I don't know the timescale on them, but I'm guessing it’s probably out there.

The other thing we didn't touch on is that this discussion has inherently been surrounding early cancer detection, but early detection more broadly is also very exciting. There are use cases outside of oncology, and I'm interested to see where this early detection activity is increasing. There is great unmet need for early detection in many areas. We are seeing a bit of this activity now, but I imagine it will increase.

.png)

.png)